Small and medium enterprises.

Private Equity and Venture Capital Firms.

M&A teams of large corporations.

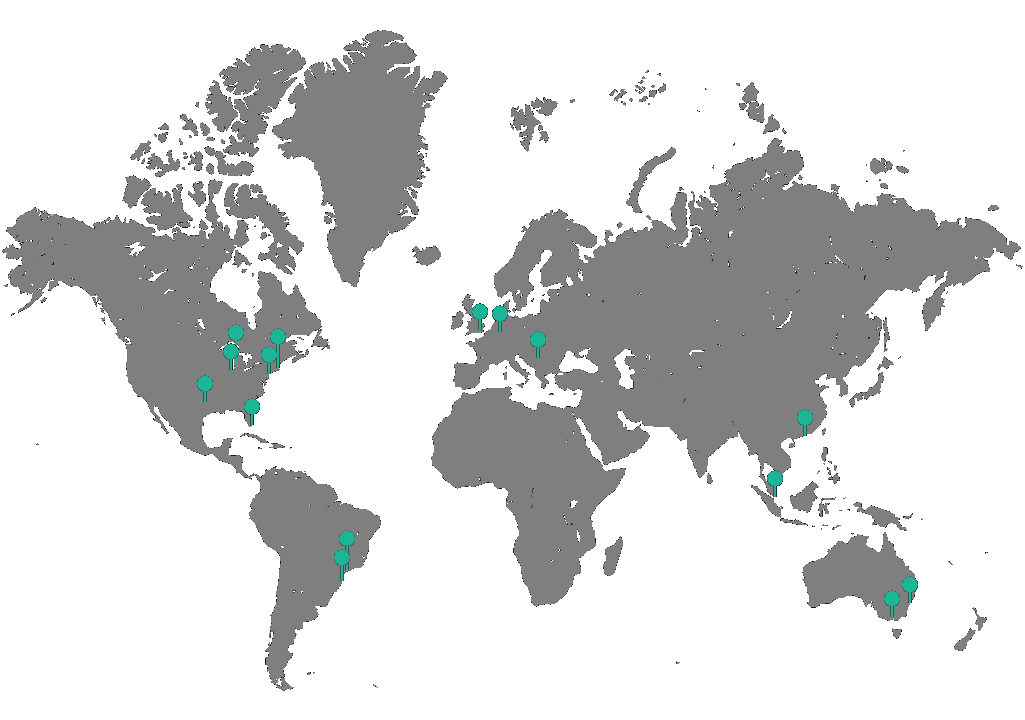

Fusion currently serve 9 markets from 7 underwriting / distribution hubs, across 4 continents.

This footprint is growing quickly.